Buying health insurance is not a luxury but a necessity. Especially in India, where the average medical inflation (14%) [1] is double the retail inflation (6.50%) [2]! During the fiscal year of 2021, health insurance coverage was provided to approximately 514 million individuals throughout India. Out of this total, around 75% of Indians were enrolled in the Indian government health insurance schemes, while individual health insurance plans covered the lowest number [3].

Health Insurance Buying Guide: From Choosing to Claiming

Evidently, as a developing nation, while India does face the challenge of providing healthcare at an affordable premium, another concern is the awareness about the need, choice, and maintenance of health insurance for individuals and their families. Queries like 'What is health insurance?', 'Which is the best insurance health policy?', 'How much health insurance premium should I pay?' inundate the internet. Even if one has health insurance, they might be concerned about the best way to renew health insurance to avail of offers/discounts. Or not sure that if they are not satisfied with their health insurance provider, they can switch the company using the health insurance portability feature.

These are what we discuss in this guide on health insurance, where we cover the entire journey from consideration and purchase to the renewal of health insurance. We'll also look at how to make the right claims for health insurance. And lastly, our recommendations on where to get the best deal on your health insurance.

But before we start our journey, let's kick off by clarifying the definition of health insurance.

Health Insurance - Definition

Health insurance is a type of insurance coverage that helps to cover the cost of medical and surgical expenses incurred by an individual. It is provided by private firms or government organisations in return for a recurring or lump sum fee (commonly termed premium).

There are different types of health insurance, such as individual health insurance, family health insurance, group health insurance, and government-sponsored health insurance. It is important to choose the right type of health insurance based on one's individual needs and budget to ensure adequate coverage and financial protection in the event of illness or injury.

Buying a Health Insurance

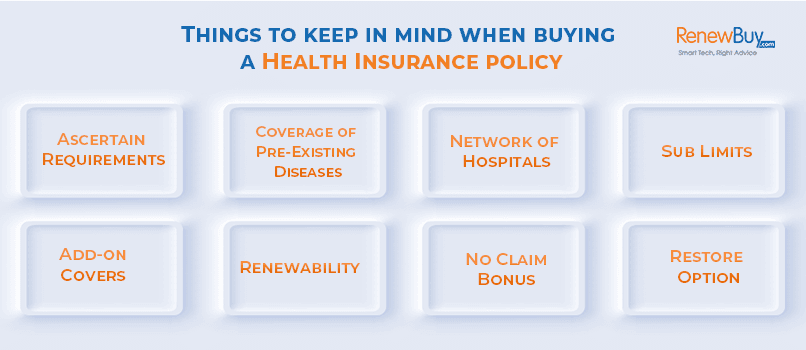

Many understand the importance of insurance in our lives, but few understand its nuances. Buying insurance is not child's play, and with the presence of so many insurance companies offering various plans for each insurance, it has become more confusing, if nothing else. Out of all the insurance policies, one policy that everyone must have in the present times is that of health insurance. Thus, the things to keep in mind when buying Health Insurance become all the more important.

Inflation in medical expenses is growing exponentially, and that too every year, and thus, getting the best treatment can become unaffordable sometimes. This is why a health insurance policy is needed. In medical insurance, too, there are several kinds of plans available, and thus, one has to understand their exact requirements to know which plan will suit them the most. However, with the umpteen options available, there are some basic guidelines and things to keep in mind when buying a Health Insurance policy.

Ascertain Requirements

The medical requirements of the family members and their age must be considered when buying health insurance for the family. A young couple planning to have a baby need to consider the maternity bills, whereas some need to take care of the requirements of the ageing parents. Lifestyle diseases are on the rise; thus, a sufficient cover keeping in mind the inflation, must be chosen.

Sum insured must be chosen wisely, keeping several factors in mind and also accounting for rising medical costs.

Coverage of Pre-Existing Diseases

Most health insurance policies do not cover any pre-existing diseases from the date of policy inception and have a waiting period of 2-4 years for certain listed treatments like piles, fissures, gall bladder stone surgery, cataract, etc. This implies that there will be no coverage if there is any hospitalisation during the waiting period for any pre-existing diseases. Some plans also have a waiting period to provide maternity cover, and thus, young couples should be careful about this clause.

However, some plans also cover pre-existing diseases, maybe with a co-payment or a slightly higher premium.

When choosing a medical insurance policy, one must choose a policy with a low waiting period. Also, if you have an existing health plan where you have completed the waiting period, do not forget to port the same when changing policies or insurers!

Network of Hospitals

The biggest advantage of buying a health insurance plan is that one can get treated in hospitals without paying huge bills from their own pocket. The cashless treatment is only available to the insured from one of the network hospitals of the insurance company.

This makes it imperative to choose a policy with many network hospitals, including the one close to the house with good medical facilities and the one that is preferred for being treated.

Sub Limits

Some health insurance policies have a sub-limit on the room rent, ICU charges, doctor fees, etc. which is predefined as a percentage of the total coverage. For example, if you have a health plan of INR 5 lakhs with a room rent capping of 1%, then your hospitalisation coverage will be provided for rooms to INR 5000 per day. Suppose you choose to stay in a room where the rent is more than INR 5000 per day. In that case, the remaining amount will not be covered. All other expenses will also be deducted from the total billing on a pro-rata basis, even though the total billing might be way lower than the coverage limit!

However, there are some health plans which have no sub-limits. Thus, if you have a health plan of INR 5 lakhs and your hospitalisation expenses are INR 1.5 lakhs, then the entire amount will be paid, irrespective of the amount of room rent you choose!

Thus, you need to opt for a plan with higher sub-limits or no sub-limits at all so that you can choose the type of room you prefer to stay in your choice of the hospital!

Add on Covers

Each insurance policy for health has the option to opt for add-on covers and riders. These optional coverage options can be availed by paying an extra premium. One must know about all the options available and choose the ones they think will be used.

Options like riders for critical illness are the ones that can be opted for as they can come in handy if needed.

Renewability

Policies can have an age limit till which they provide coverage. It is known that there are higher chances of falling ill later in life. Thus, a policy with maximum age coverage is the ideal choice. There are also options to buy family floater policies to cover their dependent parents.

Most health plans are lifetime renewable plans, and these must be the first choice when buying health insurance for the family.

No Claim Bonus

No Claim Bonus is a clause that one must check in their health insurance policy. In some policies, it can be an annual free health check-up and some shopping vouchers, whereas in some, it can be an increase in the sum insured for every claim free year.

The No Claim Bonus comes in handy in that year when your hospitalization bills suddenly shoot up and so choosing a plan with a healthy no-claim bonus is a good practice!

Restore Option

The restore option is offered by many insurance companies in their health insurance policies. Under this option, paying an extra premium can restore the sum insured if it is exhausted and hospitalisation is needed again. Thus, if you have a policy of Rs. 5 lahks and the bill is Rs.3 lakh, it will be paid under the policy. Now, if due for some reason, the insured is hospitalised again after 6 months and the bill again is 3 lakhs, it will be paid by the company as the sum insured will be reset to 5 lakhs after the first 5 is exhausted.

The restore option comes in handy for someone who has some problem and might need frequent hospitalisation and also for those who have a family floater policy.

Having a clear understanding of the policy concerning the inclusions and the exclusion is essential to get the best out of it. While selling, some aspects cannot be disclosed and thus, one should compare policies and understand the fine print.

There are many options available today when buying a health insurance policy. One must compare all and see which suits their requirements the most. Policies can be compared online on insurance aggregator websites, which help to compare easily. The importance of a good medical insurance policy is only understood when there is a need to file a claim, and sometimes, realising the mistakes then can be too late. Thus, one should be careful and use the above points to buy a good policy.

With these critical considerations of your health insurance requirements and offerings by various health insurance companies in India, you can choose the one best suited for you. Now as you buy it and go along paying the premium (while hoping no medical emergency befalls), you should pay some attention to evaluating your existing health insurance coverage. Below we discuss the main factors to consider.

Evaluating an Active Health Insurance

It is quite common for policyholders to end up availing of health insurance in India without prior research or understanding of the benefits and regrets later. This happens mainly due to carelessness or persuading pressure from the insuring companies. It also leads to complete dissatisfaction among the individuals willing to terminate or dump the policy in the long run. However, the first question that comes to our mind is: Is it possible to dump our policies before the expiration of the tenure?

The answer is YES!

However, there are several procedures involved. One must also understand the amount of return will not be as it was promised during the proposal.

Pressure from insuring companies

Approximately 60% of the policy bearers are unsatisfied with the policy benefits offered by health insurance, with a greater percentage of people being above 60 years of age. The primary reason for dissatisfaction with health insurance in India results from policies bought without prior research. This also happens in case the policyholder buys an insurance under the pressure of an acquaintance or agent who fails to put both the pros and cons on the table.

Room rent sub-limits

Room rent sub-limits refer to the maximum value an insurer has to pay for room rent. For example, for a policy of 4 lakhs, INR availed 20 years ago, charging 1% of room rent every day will be subject to 4000 INR charged every day. If this occurs, search for alternative health insurance cover for the best is better.

Unexpected renewal hikes

Renewal hikes are also one of the important reasons for dissatisfaction by people, mostly belonging to the group of senior citizens. In many cases, the premium of renewed health insurance plans surge manifolds which crosses the expected annual premium value. Sometimes, it becomes unaffordable for the policyholder to continue the premium leaving the policy bearers with no choice but to let it lapse. It is highly recommended to the policyholders that any surge in the annual premium rates that crosses the pre-settled or expected value must be monitored and terminated when not convenient for them.

Expected refund in case of No-claim Bonus

People are solely advised to opt for the best health insurance that suits their needs completely. However, if unsatisfied, premiums covered under health insurance plans terminated within a certain period of time can be refunded by the insuring company, provided the terms and conditions are followed wisely. Though the sum cannot be completely refunded, much of the amount depends on the period within which it is being claimed and prior claims of benefits made in history. Policyholders who have not made any claim of policy benefits within the tenure of the policy can successfully claim a refund while dumping the health insurance policy.

The refundable amount, however, depends on two factors-

Free look period: Any health insurance plan can be dumped or suspended within a free look period. The free look period is the time interval of less than a month (approximately 15 days) after buying the policy, within which the policyholder can successfully avail of the maximum refundable amount. Apart from the stamp charges and the administration fees, the insuring company returns the entire sum of the premium submitted.

Within The First Year Of Policy: In case a policy bearer wishes to dump the health insurance policy and expects a refund of a certain amount of the premium, it is best to terminate within the first few months. With the increase in the policy period, the percentage of refundable money keeps on decreasing. The amount refunded by the insurer within the first month of the policy is greater than that returned after 3 months, which is again greater than the one refunded within 6 months. After 6 months, generally, no amount will be refunded.

Co-Paying alternatives

Co-paying can eat a huge chunk of the health insurance policy. It is mostly stated for certain diseases, surgeries, and conditions which is not completely covered by the insuring company and might lead to a huge amount subjected to payment by the policyholder.

The health insurance coverage provided by the insuring companies always comes with a set of rules and regulations. This also includes clauses and conditions for terminating and suspending a health insurance policy before its expiration. Such conditions should be checked twice before signing the proposal. However, the policyholder should double-check the benefits in the first place and agree to the policy only if it suits his/her needs completely.

Now, say the health insurance assessment tells you that despite your insurance provider being good, th health insurance you have purchased may not be enough. Then you can upgrade your health insurance!

Upgrading an Active Health Insurance

Health insurance is vital. It protects against medical costs arising from hospitalisation, diagnosis, and treatments. With an average cover ranging between Rs. 2 lakhs to Rs. 5 lakhs, it serves as a financial cushion in times of medical emergencies. Yet very often, policyholders find this amount inadequate to meet emergencies. Rising inflation has pushed the cost of medical treatments to skyrocket high. Actual expenses may far exceed your existing health insurance coverage. Thus, the policyholder may have to shell out the difference from his pocket, which defies the very purpose of health insurance.

So, here we will discuss all you need to know about upgrading your existing Health Insurance Coverage.

Enhancing your sum assured with a super top-up plan

Super top-up plans have stemmed from a policyholder's needs which enhances their existing sum assured to meet the rising cost of medical care. A super top-up plan is typically an add-on plan that could be purchased over and above your basic health coverage. An easy and cost-effective policy lets you upgrade your existing health insurance coverage. to meet the expenses.

By buying a super top-up plan, the additional cover that you would receive is paid out only if your expenses have crossed a pre-determined limit known as the "deductible or threshold limit".

Deductible and threshold limit - how does the policy work?

Super top-up plans work around a deductible or threshold limit. Specified at the time of purchase of your super top-up plan, it is that amount over and above which the super top-up plan would entertain your claims. So, you would typically need a basic health insurance policy for expenses below the threshold limit.

Look at this example: Let us consider a health insurance policy with a basic sum assured of Rs. 2 Lakhs. A super top-up policy of Rs. 10 Lakhs is purchased to enhance this cover. At the time of purchase, it is pre-determined that the deductible or threshold limit is Rs. 2 lakhs. Let us look at three scenarios to understand how claims would be paid out in such a case.

Scenario 1: A claim of Rs. 2 lakhs due to hospitalisation

The claim amount would be paid out from the regular health insurance policy. The super top-up policy does not kick in as:

- The amount is well within the scope of the base health insurance policy,

- The threshold limit for the top-up to kick in has not been reached.

Scenario 2: A claim of Rs 8 lakhs arises due to hospitalisation

In such a scenario, it is obvious that the base health plan with a cover of Rs. 2 lakhs would not be adequate. The existing base health policy would provide cover as per its terms for Rs. 2 lakhs. The super top-up plan kicks in once the bills exceed the pre-decided threshold limit of Rs. 2 Lakhs, up to the sum assured amount.

So, in this case, the balance amount (8lakhs-2 Lakhs) of Rs. 6 lakhs would be paid by the super top-up plan.

Scenario 3: A claim of Rs. 12 Lakhs

Where the claim amount is higher than the regular policy and the super top-up policy put together, a certain amount would have to be borne by the policyholder. As in the scenario, in the claim of Rs. 12 lakhs, Rs. 2 lakhs would be taken care by the regular policy. The super top-up policy would settle claims up to Rs 10 lakhs.

So, the balance amount of Rs. 8 lakhs is taken care of by the super top-up policy. The remaining Rs. 2 lakhs would have to be borne by the policyholder.

The cost factor

The most cost-effective option is a super top-up policy when you want to upgrade your existing health insurance coverage. Instead of purchasing another new policy, top-up policies are far easier and hassle-free. Premiums are far more affordable in comparison to a regular health policy. The premium you would be paying depends upon the deductible decided upon.

- Buying from another insurer: Super top-up plans need not have to be bought from the same insurer as the basic health policy. You could buy both from different insurers.

- Individual and family floater plans: Super top-up plans could be bought as an individual plan or as a family floater plan covering spouses and children.

- Super top-up plan Standard Waiting Period: A super top-up policy's waiting period and exclusions are similar to a regular policy. Policies come with a 3- 4 year waiting period for pre-existing ailments coverage.

Designed to meet the increased costs of medical care, super top-up plans work towards upgrading your existing health insurance coverage. So, when inflation pressures are high, you could upgrade your existing health plan to ensure it covers you adequately. Once you are aware of all you need to know about upgrading your existing Health Insurance Coverage, it is much easier for you to opt for a plan.

There you go with what all you need to assess and upgrade the coverage when your health insurance is still active. Next, whether you avail a claim or not, your health insurance is going to expire as it comes with a duration limit - typically in a year. In that case, if you don't renew your health insurance timely, it will lapse. Meaning you will lose all the coverage, benefits and discounts you were getting from your insurance provider. This is critical to understand as the gap between lapse and renewal of health insurance could mean falling in a medical emergency without a safety net.

Below we lay out the situation and solution to deal with the lapse in a health insurance policy.

Dealing with a Health Insurance Lapse

A health insurance policy comes with a fixed tenure. Normally, this tenure is for a period of one year. But what to do when a health insurance policy lapses? Nowadays, health insurance plans come with longer durations as well. There are plans which you can buy for a continuous period of two or three years by paying the two-year or three-year premium at once. These long-term plans not only eliminate the hassle of annual renewals but also lower the premium cost too because there are premium discounts for choosing longer durations. However, even in the case of long-term health plans, renewals are required when the policy duration comes to an end. Your health insurance policy lapses if you do not renew the plan on time.

Let's find out what to do when a health insurance policy lapses and how it affects the policyholder.

What is a lapse in a Health Insurance Policy?

If the health insurance policy is not renewed before the policy expiry date, the policy will lapse. A lapse of the policy means termination of health insurance coverage. If the health insurance policy lapses, the available coverage under the plan comes to an end. In case of a claim in a lapsed policy, the insurance company does not pay a single penny as the cover has stopped.

What to do when a Health Insurance Policy lapses?

If your health insurance plan has lapsed, you should pay the renewal premium as soon as possible to renew the plan with existing coverage benefits.

Related Article: What To Do When A Health Insurance Policy Lapses?

Grace Period Renewal

There is a grace period in health insurance plans. This period allows the payment of renewal premiums after the policy has lapsed. Most health insurance plans offer a grace period of 30 days. If the policy has lapsed, but you pay the renewal premium during the grace period, you can restart the policy. The continuity benefits of reduction in the waiting period and no claim bonus would be applicable in such a policy that was renewed during the grace period.

Though a grace period is allowed for reviving a lapsed health insurance policy, the grace period does not allow coverage. If any claim occurs, the company will not pay any benefits even when the policy is in the grace period.

Why a Health Insurance lapse should be avoided?

It is always better to renew the health insurance plan before it lapses. A lapse should be avoided because of the following reasons -

No coverage in the interim period

There is no health insurance coverage in a lapsed policy. These expenses could burn a hole in your pockets given the high medical costs.

Portability

A lapse prohibits your ability to port to a different company. If you want to change your health plan because of any service issue or better coverage features or any other reason, you lose the ability if the health insurance policy lapses. The request of porting should be made 45 to 60 days before the policy expiry date and not after the expiry of the policy period.

Renewal benefits

If the policy is not renewed during the grace period, you lose the renewal benefits of your existing health insurance plan.

Waiting period

In case of a lapse, you lose the continuity benefits of the waiting period on pre-existing diseases. The reduced waiting period for pre-existing illnesses and other treatments. You would, then, have to buy a fresh health insurance policy with a fresh waiting period of two to four years or as defined by the underwriter.

Limited scope of new policy

If you are a senior citizen, you might find new health plans to have a limited scope of coverage than your lapsed health insurance plan. Even for others, your new ailment might not be covered under the pre-existing clause, which would have otherwise been so in your previous plan.

Lifelong renewability

Moreover, lifelong coverage is allowed only if the policy is renewed without a break. If the policy is not renewed within the grace period, you might not find a health insurance plan for your age.

No claim bonus

Even the accumulated no-claim bonus for not claiming in the previous years would be lost if the policy is not renewed on time.

Steps to ensure that you do not lapse your Health Insurance Plan next time

- Update your email id and phone number accurately with the insurer and update the same in case of a change, so that you do not miss renewal calls, emails, etc.

- You can also create a standing instruction on your account, credit card, etc., so that the renewal gets automatically processed even if you are busy or out of the country or unable to pay within the grace period. This way, you can never miss your renewal lifelong!

How to Renew Lapsed Health Insurance Policy?

However, if your health plan has not been renewed and has lapsed beyond the grace period, all you need to do is buy a fresh plan. Since the same cannot be renewed now, you can either continue the same plan with your earlier insurance company by simply paying the premium and undergoing a pre-medical check-up if the lapse is more than 6 months or compare and then buy a fresh health insurance plan for yourself which suits your needs the best.

With the technology on our side, there is no excuse for missing renewal payments. It can be done seamlessly through net banking, phone banking, app banking, etc., and just with the click of a button.

So, far we know the best practices for buying, evaluating, and renewing health insurance. It's time to touch upon health insurance claims - as, however, unpleasant - is an integral part of the health insurance journey. We don't wish it comes to that but if it does, below is what you need to do to avail the features, benefits, and coverage of all the health insurance premiums you paid.

Claiming Health Insurance

Typically, in a health insurance claim, the insurer asks the insurance provider to make the treatments covered by their policy available in accordance with the insurer's needs. This further resolves the issue of selecting the kind of health insurance claim that would offer the greatest medical benefit. The claimant then has the choice of making a cashless claim or a reimbursement claim.

Cashless Claim

In this case, the relevant insurance company will be liable for paying the hospital's bill for any expenses incurred following the insured's medical treatment. Because of the insurance company's relationships with hospitals, submitting a claim for medical care through them is generally secure. Hence, the patient is spared the discomfort of having to withdraw cash in an emergency.

However, in order for the claim process to go well, one must ensure that all of the terms and conditions of the health plan are carefully reviewed and accepted before filing a claim for any type of health insurance.

Reimbursement Claim

In contrast to a cashless claim, where the insurance company has impaneled hospitals, a reimbursement claim allows the insurer to select any hospital for the medical treatment, even if it is one that is not on the insurance company's list of approved hospitals. Yet, in this case, the insured must cover all associated medical costs before requesting reimbursement. To make use of this specific claim, you must give the insurance provider all necessary paperwork, including the first invoices. They may only continue with the payment of the accumulated medical invoice after confirming the documents in accordance with their own company's policy.

Nonetheless, the insurance provider has the right to reject the claim if, for whatever reason, the essential treatment does not fall under the purported insurance or is not covered by it.

Therefore, reading the terms and conditions of any claim process before submitting it is advised.

Most commonly, there are standards established to ensure health insurance. There are too many documents needed when applying for health insurance. This serves as an assembly for proofs for the application. Luckily, digitization has reduced the amount of paper shifting and made things easier for applicants.

Even with the use of technology, one must still submit these documents in order to complete the task. Typically, below is the set of documents one should be ready with in order to avail of healthcare insurance.

Health Insurance Claim Documents

1. Age proof: The first and foremost requirement while buying health insurance. It can be a-

- Voter ID Card

- Pan Card

- Aadhaar Card

- Driving License

- Passport

- Birth certificate

2. Identity proof: This is necessary for documenting the records, which will further benefit the coverage offered to the insured.

- Voter ID Card

- Passport

- Aadhaar Card

- Driving License

3. Address Proof: Your health insurance company will send various communications on your postal address. You can also submit any of the following for verification:

- Ration card

- Driving license

- Passport

- Rent agreement if applicable

- PAN Card

- Aadhaar Card

- Utility bills like electricity bill, telephone bill, etc.

4. Passport-size photographs (on insurer's demand)

5. Medical reports (on insurer's request)

6. Proposal form duly filled in and signed

*Disclaimer: the documents mentioned above are pointed in general. Sometimes the insurer may have different document requirements. Therefore, the list may vary.

Securing your health means securing your future, and having health insurance further solidifies your take on life as you venture well-armored. Health is wealth. So, choose your healthcare policy now and get insured for life.

Health Insurance Claim Process

The procedure to avail cashless claim for a health insurance policy includes the following steps:

- Contact the insurance help desk at the hospital.

- Verify the identity by providing the ID card provided by the insurer.

- Once the verification process gets completed, the hospital provides a pre-authorization form to the insurance provider.

- The insurer then reviews the submitted documents and processes the claim according to the terms and conditions of the policy.

- Some health insurance companies also provide a field doctor to make the hospitalization process easier for the insured.

- Once the formalities are completed, the claim is settled as per the terms and conditions of the policy.

With that, we are at the last leg of our journey to understand the life cycle of health insurance in India. Aware and motivated, we hope you are ready to buy health insurance for yourself and your loved ones. You can buy health insurance both online and offline. Given the hectic routine of daily life, it's convenient to do so online. But even in online health insurance purchases, you have two options: either buy directly from the insurance company website or from the insurnace comparison website like RenewBuy.

RenewBuy offers a stop solution to all your queries, comparison, and service required to help you throughout your health insurance journey. From expert advice on picking the right health insurance, availing the attractive deals on premiums, assisting in a smooth claim process, and more. Below mentioned are the steps to buying the best health insurance plan in India with RenewBuy.

- Visit the official website of RenewBuy.

- Click on the "Health Insurance" tab.

- Fill out the form that shows on the next page.

- Compare health plans and select your desired plan.

- Click on the "Buy Now" button

- A pop-up will show you the plan details and the additional riders' information.

- Click on the "Proceed to Buy" button.

- Make online payment, and the policy documents will be sent to your registered email address.

Key Takeaways

There you go with the end-to-end view of the health insurance journey in India. Buying health insurance can be one of the smartest decisions you can make for yourself and your family. In today's day and age, lifestyle and environmental changes have led to a complete shift in people's health dynamics. Although the medical infrastructure in the country and the world keeps improving, the treatments and facilities cost much higher. Having health insurance by your side takes off all your worries about any kind of financial pressure, and you are free to choose the best treatments for yourself and your loved ones.

Share this article

Related Article

Lung Cancer: Symptoms, Diagnosis,.....

Overview Lung cancer is one of the most common and severe types of cancer. It involves the uncontrolled growth of.....

Read Full Blog

Sep 24, 2025

Health Insurance Claim Settlement.....

Health insurance can help us avoid financial stress, an important lesson the pandemic has taught us and continues to teach.....

Read Full Blog

Sep 1, 2025

What To Do When.....

A health insurance policy comes with a fixed tenure. Normally, this tenure is for a period of one year. But.....

Read Full Blog

Apr 25, 2025

What is Co-pay, Deductible.....

When it comes to availing health care insurances and schemes, it is difficult to understand all the terms and their.....

Read Full Blog

Aug 26, 2025

Janani Suraksha Yojana: Features,.....

In India, access to quality healthcare during pregnancy and childbirth remains a major challenge, particularly for women from underprivileged backgrounds......

Read Full Blog

Sep 15, 2025

Mukhyamantri Amrutum Yojana

the Gujarat government, led by Mr Narendra Modi, launched the Mukhyamantri Amrutum Yojana. In August 2014, it was extended to.....

Read Full Blog

May 2, 2025

CMCHIS - Chief.....

Chief Minister Comprehensive Health Insurance Scheme is popularly known as CMCHIS. CMCHIS was launched on 11th January 2012 by the.....

Read Full Blog

May 16, 2025

Star Health Insurance Renewal.....

Health insurance becomes essential thing in our life as it provides financial protection in case of medical emergencies. It is.....

Read Full Blog

May 16, 2025

Mukhyamantri Chiranjeevi Swasthya Bima.....

Mukhyamantri Chiranjeevi Yojana was inaugurated by the Chief Minister of Rajasthan Mr Ashok Gehlot, and it was launched in the.....

Read Full Blog

May 8, 2025